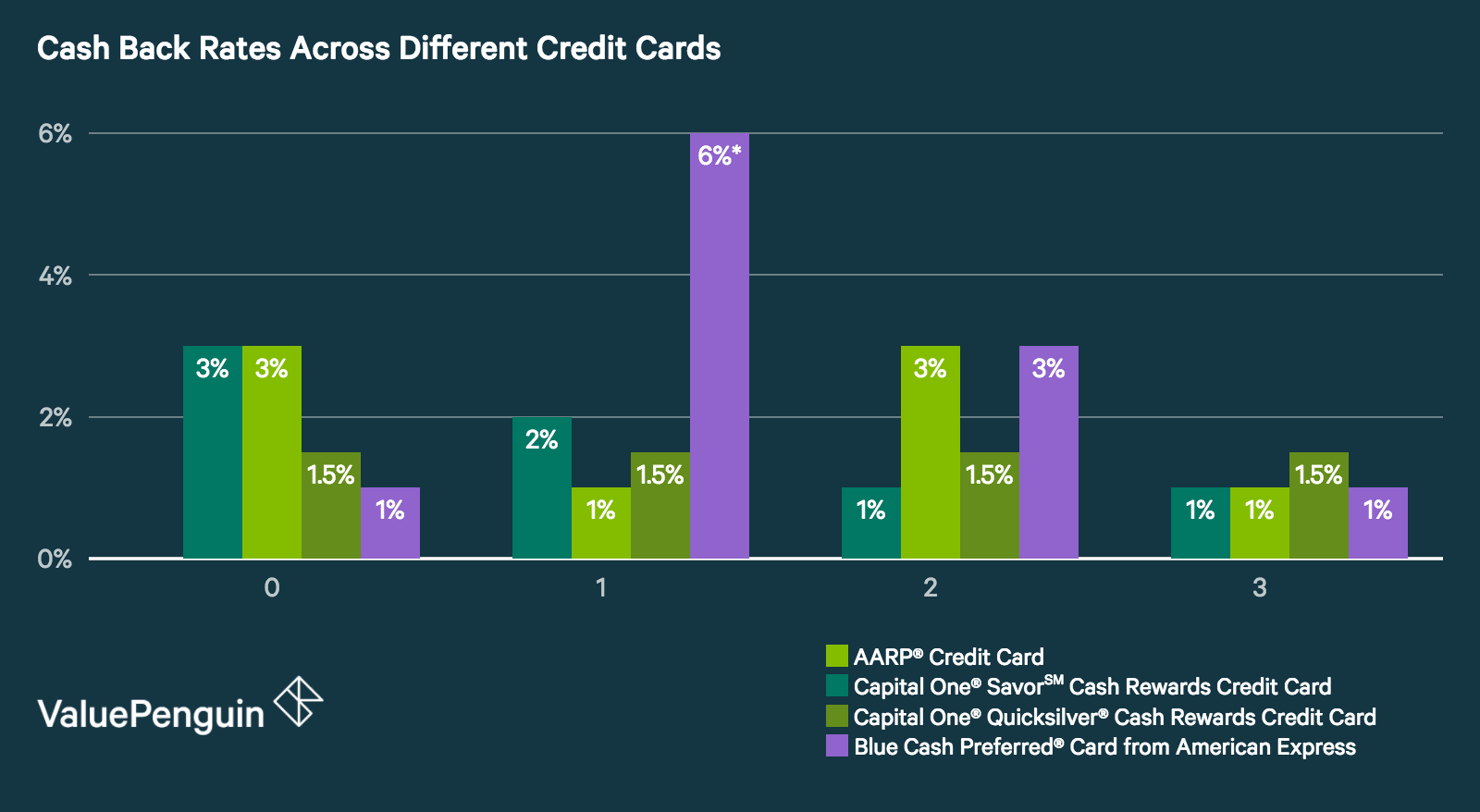

One financial will proudly state they have a passion rates off 3

One financial will proudly state they have a passion rates off 3

Whenever asking home loan companies because of their costs, it’s all using number up until it make suggestions the great believe guess. 5% when you’re an alternative get an interest rate from 3.9%. Exactly what the bank to your down speed usually don’t explore without searching better is the fact that doctor acquiring the financing was probably buying issues to their financial.

Paying off affairs is an approach to spend currency at the start for a reduced rate of interest. It barely looks like in your favor.

Good faith quotes clearly listing aside rates of interest, charge because of the financial, and 3rd area charge (particularly review, questionnaire, or any other requisite data that the customer can also be shop around to have).

If you don’t see a good-faith estimate, the fresh new % rate is likely simply an intro to attract your in the. Sometimes a minimal stated rate is not necessarily the most affordable loan solution as fees can be extremely high.

Never Assume Huge Deals

Shortly after considering good-faith prices, there’s the exact same thing that i performed. For every providers practically got equivalent will cost you.

After bidding the great trust rates facing both, However found the lowest buyer. Finally, We wound up protecting $700 http://cashadvancecompass.com/payday-loans-la from the hunting 6 different mortgage people. Once you figure that evaluation of the property will most likely run $five-hundred or other fees are near to $5,000, the latest deals appear some brief. I was expecting far more type if you find yourself to acquire a home to have well on the half dozen data. Financial cost are set as there are such competition currently you to definitely what you shell out regarding bank so you can bank may not will vary by the a huge amount.

You are Nevertheless Using PMI

DI, otherwise private financial insurance. How financial will get to PMI should be to improve charge or hobbies cost satisfactory so you can blend new PMI with the life of the loan. Essentially, youre nevertheless expenses PMI, simply it may never ever subside. It would be there into the longevity of the loan, while making a doctor financial a potentially higher priced home loan over the long run.

Believe an arm

Changeable speed mortgages (ARM) acquired loads of bad visibility as much as 2008-nine in home loan crisis. Today, many people are terrified discover a supply because of all the this new crappy publicity.

I’d believe a health care professional financing just could be an excellent prime candidate having an adjustable speed financial (ARM). That it assumes that the doctor is going to continue practicing, recently graduated from property otherwise fellowship, and will prevent too-much purchasing. Here you will find the reasons why I sometimes suggest having an arm to have medical practitioner money

Mortgage cost tend to typically keeps straight down passion rates compared to 30 seasons repaired.

Really the fresh new likely to medical professionals (and non physicians) does not remain in its first family longer than 5 to seven many years.

Safe employment market. Though a physician will get let go away from a group due to help you an excellent takeover. There are always locum tenens or any other services which can with ease be found. This can be false with other industries in which it takes per year or more to find an identical business..

First a good example of costs that i gotten regarding the exact same lender. Lets guess a good $440,000 cost that have 5% off. The 2 also offers had been:

3.4% desire towards a great 7/step 1 Arm

cuatro.4% desire to the a 30 12 months repaired

Charge to your Sleeve financing was indeed in reality $1,000 less expensive than 30 year repaired.

Regarding Case financing a family doctor is purchasing $63,100 theoretically and you can $93,138 towards the focus over 7 age before the loan rates resets. Total leftover harmony into the loan at the eight decades are $336,900